Apple (AAPL) is unique among America's mega caps due to the company's ongoing rates of revenue and earnings growth. From $108.25 billion in revenue reported in the fiscal year ended in September, Apple will surpass $170 billion in revenue this fiscal year and reach over one-quarter trillion dollars in revenue in FY2013. At a current market cap of $375 billion, the shares trade at about 14.5 times trailing twelve month earnings of $27.68 per share and at about 8.75 times my projected FY2012 earnings of $46 per share.

Because of the company's frenetic rates of revenue and earnings growth, Apple is in an equity class all its own. Apple will deliver a third consecutive fiscal year of revenue growth above 50% and eps growth above 60%. This fiscal year's strong performance begins with what I call "Apple's monster quarter."

Apple's Monster Quarter

Apple's first fiscal quarter of FY2012 will be fourteen weeks in length. It stretches from September 25, 2011 to December 31, 2011. The additional week in the quarter will encompass the immediate post-Christmas period. The quarter also includes the initial release of the iPhone 4S in the United States and other launch countries. The additional shipping week, the new Sprint agreement for the iPhone and pent-up demand for the recently refreshed smartphone handset will deliver revenue growth greater that 60% in the quarter and eps growth exceeding 80%.

AAPL's Discount To Current And Future Growth

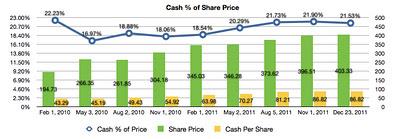

The chart below illustrates how much the rate of Apple's share price appreciation has fallen behind the rate of earnings growth over the past four quarters. Despite the 82.7% growth in earnings per share in FY2011, at Apple's closing price of $403.33 on Friday, December 23rd, the share price has risen only 24.64% year-over-year. The dates selected for the charts in this article represent the first trading day of the month following the release of quarterly earnings and the closing price on Friday, December 23, 2011.

A more dramatic illustration below indicates Apple's price-earnings multiple has fallen in an inverse relationship to the rising cash per share over the past 22 months.

Rising cash coupled with a falling price-earnings multiple indicates a market expectation Apple's rates of revenue and earnings growth will soon begin to slow. There's a disconnect between the perceived limits to Apple's continuing strong growth and the reality of the company's potential for growth. Apple is the quintessential enterprise growth story of the new millennium.

Over the past 18 months, cash per share has steadily risen as a percentage of the share price. The market has continued to discount Apple's potential for organic earnings growth despite the company's consistently strong financial performance.

The Market Misread Of The Apple Growth Story

In a recently posted article titled Where Apple Makes Its Money, I explored the company's potential for continued revenue and earnings growth through global expansion. Apple is currently addressing only a fraction of the global market for the company's digital lifestyle products. By FY2013, two-thirds of Apple's revenue will be sourced from regions outside of the United States with strong growth fueled by product sales in currently underserved markets.

The only practical limits to Apple's revenue and earnings growth over the next two years have nothing to do with competing products despite media efforts to create sales contests. Rather, Apple's rates of growth will be governed by how quickly Apple can expand its product sales presence in currently underserved markets such as China, Brazil and India and how quickly the company can expand production to meet incessant global demand.

Apple's Pending Share Price Advance

The current Street consensus for FY2012 calls for revenue growth of 28.8% to $139.40 billion and earnings growth of 25.6% to $34.77. For FY2013 the consensus estimates are even more perverse. These estimates not only discount Apple's potential for growth in currently underserved markets, the estimates suggest these markets don't exist. Apple's annual eps growth rate will remain above 50% through FY2013.

The December Quarter Outcome

In addition to the 14-week December quarter, reported iPhone sales will benefit from the initial release of the iPhone 4S early in the period. Apple's decision to migrate the new handset's release to the December quarter not only dampened September quarter results, it moved the release to the next fiscal year.

Indicated by the graphs above, Apple's price-earnings multiple contracted in 2011 as share price appreciation lagged behind the pace of growth in earnings. The share price will begin to recover as the calendar moves closer to the release of the December quarter results and Apple signals to the market the rates of revenue and earnings growth realized in fiscal years 2010 and 2011 will continue for a third consecutive year.

Although geo-political and macro economic factors impacted Apple and the broader market during 2011, the release of the iPhone 4S in the December quarter put additional pressure on the share price in late summer and fall. The September quarter results absent the iPhone refresh stalled share price appreciation in the fourth calendar quarter, leading to a sustained contraction in the price-earnings multiple. The amplified December quarter outcome and the revised analyst estimates for FY2012 and FY2013 that will immediately follow are the catalysts for share price appreciation this winter.

Conclusions

I maintain a $640 price target on the shares. A recovery to a trading range between 16 times and 18 times trailing 12-month earnings will occur early in 2012 following the results from "Apple's monster quarter" and the significant analyst upgrades to revenue and earnings estimates that will follow. The sales performance of the iPhone 4S and the anticipated late winter/early spring refresh of the iPad line will be share price catalysts in the first half of the current fiscal year. But it's Apple's continuing push into previously underserved global markets that will sustain the share price advance in the latter half of FY2012 and early FY2013. Apple has passed its share price nadir relative to earnings and my models forecast a breakthrough above $500 per share by early April 2012. The December quarter outcome will move trailing 12-month earnings to over $32.50 per share.

Apple's twin drivers for growth are product innovation and continued global expansion. Both drivers will move the share price dramatically higher in FY2012.

Robert Paul Leitao

Disclosure: The author is long AAPL shares

penn state riot penn state riot state college pa wilson ramos kidnapped mcqueary mike mcqueary joe paterno fired

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.